Protecting a jewelry store with a standard business insurance policy is like using a simple padlock to secure a bank vault. It just doesn't cut it. Your business demands specialized coverage from jewelry store insurance companies that truly understand the unique, high-stakes risks of the industry.

For jewelers, this specialized shield is called Jewelers Block insurance. It’s engineered from the ground up to protect against the sophisticated threats you face every single day.

Why Your Jewelry Store Needs Specialized Insurance

A typical Business Owner's Policy (BOP) works fine for a clothing boutique or a bookstore. But for a jeweler? It's dangerously insufficient. These general policies have critical gaps and shockingly low limits for high-value inventory like diamonds, precious metals, and finished pieces.

Relying on a standard BOP leaves you exposed to catastrophic financial loss from a smash-and-grab robbery, theft during transit, or even a fire. It was never designed to handle the value and portability of your assets.

Jewelers Block, on the other hand, is an "all-risk" policy built specifically for the jewelry trade. It bundles multiple coverages into one seamless plan, protecting your inventory whether it's locked in the vault, sitting in a display case, traveling to a trade show, or out with a salesperson. No matter what kind of business you run, understanding business insurance essentials is the first step toward real security.

Jewelers Block vs Standard Business Insurance At a Glance

The difference between a Jewelers Block policy and a standard BOP isn't just a small detail—it's a massive gap in protection. A standard policy might cap jewelry coverage at just a few thousand dollars, which wouldn't even cover a single high-end piece in your display. This table breaks down the crucial distinctions.

| Coverage Feature | Standard Business Owner's Policy (BOP) | Jewelers Block Insurance |

|---|---|---|

| Inventory Coverage | Very low limits; often excludes theft of precious stones and metals unless specifically endorsed. | Comprehensive "all-risk" coverage for your entire stock, including loose stones and raw materials, up to the agreed value. |

| Off-Premises Protection | Extremely limited or non-existent; rarely covers goods in transit, at trade shows, or with salespeople. | Explicitly covers inventory while off-site, including travel, exhibitions, and when with employees or messengers. |

| Customer Property | Typically not included; requires a separate bailee's policy to cover items left for repair or appraisal. | Automatically includes coverage for customers' property left in your care, custody, and control. |

| Mysterious Disappearance | Almost always excluded. | Often available as an optional endorsement, providing coverage for unexplained losses. |

As you can see, a BOP simply isn't equipped to handle the fluid, high-value nature of a jewelry business. A Jewelers Block policy is the only way to get true, wall-to-wall coverage.

The core purpose of Jewelers Block is to provide protection that moves with your inventory. It acknowledges that your most valuable assets are constantly in motion and exposed to unique threats a standard policy was never designed to handle.

Navigating this specialized world requires a partner who lives and breathes it. A dedicated agency like First Class Insurance focuses exclusively on the needs of jewelers, making sure your policy is structured correctly without dangerous gaps. To learn more, check out our guide on why jewelry stores need insurance. Securing the right protection is the most important step you can take to safeguard your business and your legacy.

What a Jewelers Block Policy Actually Covers

Think of a Jewelers Block policy less like a single lock on your door and more like a comprehensive security system that guards every corner of your business. A standard business policy might cover your display cases and storefront, but what about the diamonds, watches, and gemstones inside? That's where it falls dangerously short.

This specialized jewelry store insurance is built to protect your high-value assets no matter where they are. It’s known as an “all-risk” policy, which is a fancy way of saying it covers losses from pretty much any peril, unless that specific risk is explicitly excluded in the fine print.

This approach is designed for the reality of the jewelry business, where your inventory is rarely static. Whether a piece is in your main vault, on display, or with a salesperson visiting a client, the coverage follows it.

On-Premises Inventory Protection

The foundation of any Jewelers Block policy is protecting the inventory right there in your store. This is your first and most critical line of defense, safeguarding your stock against the obvious threats that can happen on your property.

This coverage wraps its arms around your entire stock, including:

- Finished pieces: The engagement rings, necklaces, and watches ready to walk out the door.

- Loose stones and metals: Your supply of diamonds, sapphires, gold, and platinum waiting for its moment.

- Items in process: Pieces being meticulously crafted or repaired in your workshop.

Picture a smash-and-grab robbery where thieves shatter your displays and make off with thousands of dollars in merchandise. Or imagine a fire breaking out in the workshop overnight, ruining both raw materials and finished heirlooms. In either case, your Jewelers Block policy is designed to cover the financial loss of that stock, right up to your policy limits.

One of the best things about Jewelers Block is how it adapts to your daily workflow. It covers your inventory whether it's out in a display case, secured in a safe overnight, or locked away in a high-security vault.

Off-Premises and In-Transit Coverage

Here’s where Jewelers Block insurance really sets itself apart. Standard business policies almost always draw the line at your front door, leaving high-value goods completely exposed once they leave. For a jeweler, that's a massive blind spot.

This coverage is absolutely essential for common situations like:

- Salesperson Travel: Protecting inventory when your employee is on the road visiting clients.

- Trade Shows and Exhibitions: Covering your stock while it's on display at an industry event.

- Shipping and Transit: Securing goods sent to customers or between locations via armored transport or approved carriers.

- Memo Goods: Shielding items you've sent to another retailer on consignment.

So, if a salesperson’s car is stolen during a sales trip, the policy would cover the value of the jewelry that was inside. If a shipment of diamonds gets lost or stolen in transit, your coverage kicks in. It’s designed to protect your assets when they are at their most vulnerable—outside the fortress of your store.

Coverage for Customers' Property

Your entire reputation is built on trust. A Jewelers Block policy helps you honor that trust by covering "property of others" while it’s in your care, custody, and control. This isn't just a nice-to-have; it's a reputation-saver.

This part of the policy covers customer items left with you for appraisals, repairs, resizing, or just a simple cleaning. If a customer’s cherished heirloom was stolen from your safe during a break-in or damaged in a flood, your insurance would cover the cost. This doesn't just prevent a catastrophic financial loss; it protects your good name.

For a deeper dive into the specifics, you can learn more about what Jewelers Block insurance covers in our complete guide. Partnering with one of the best jewelry store insurance companies means finding someone who truly gets all these moving parts.

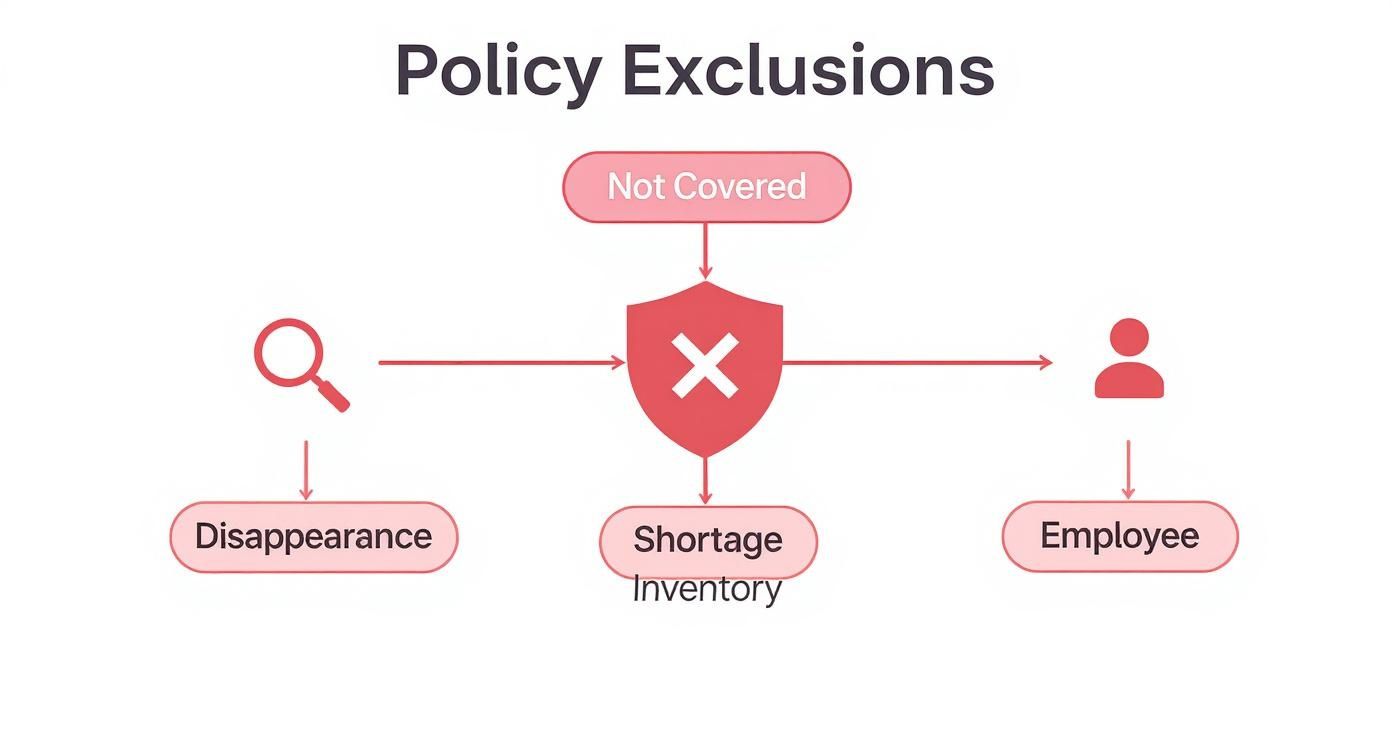

Understanding Policy Exclusions and Gaps

A Jewelers Block policy is a powerful shield, but it’s not invincible. Knowing what your policy doesn't cover is just as critical as knowing what it does. Lurking in the fine print are specific exclusions—the situations where your insurer will not pay a claim.

These aren't random "gotchas." Insurers write exclusions to manage their own risk, specifically for losses that are either impossible to prove or stem from internal failures rather than outside events. If you ignore them, you could be in for a nasty shock right when you need that safety net the most. Let's pull back the curtain on the most common ones.

Mysterious Disappearance

This is one of the most frequent—and frustrating—exclusions for jewelers. Mysterious disappearance is exactly what it sounds like: an item is missing, but there’s absolutely no evidence of what happened to it. No broken lock, no shattered showcase, and no security footage of a thief. It just…vanished.

Picture this: you’re doing inventory and realize a five-carat diamond ring from the main display is gone. You and your staff search everywhere. You check every log and camera angle. Nothing. It’s as if it evaporated into thin air. That’s a classic case of mysterious disappearance.

Why is it excluded? From an insurer's point of view, it's an impossible claim to verify. Was it a simple counting error? Did it get misplaced? Was it an inside job? Without any evidence of a specific event like a theft, it becomes an uninsurable risk. While some specialized jewelry store insurance companies might offer coverage for this as an add-on, expect it to come with a much higher premium and a hefty deductible.

Unexplained Inventory Shortage

This one is a close cousin to mysterious disappearance but usually applies on a larger scale. Unexplained inventory shortage, or "shrinkage," is the loss you discover only after a full physical inventory count. It's the gap between what your records say you should have and what you actually have.

For example, you run your year-end numbers and find your physical stock is short by $25,000 compared to your books. You can’t pinpoint a specific robbery or event that caused it; these are small, untraceable losses that have added up over months.

A Jewelers Block policy is designed to cover defined, verifiable events—a smash-and-grab, a fire, a shipping mishap. Gradual, unexplainable shrinkage is seen more as a cost of doing business and is almost always excluded.

This exclusion really drives home the importance of rock-solid internal controls. Insurers expect you to have tight processes to manage your inventory and prevent these slow-drip losses that can't be tied to a single covered cause.

Dishonest Acts by Employees

This is perhaps the most vital exclusion for any store owner to understand. Your standard Jewelers Block insurance will not cover theft, fraud, or any other dishonest act committed by your own employees.

If you discover a trusted manager has been pocketing small pieces from the safe for months, your Jewelers Block policy won't cover that loss. Why? Because the policy is built to protect you from external threats, not internal ones.

Why is it excluded? Insurers consider employee dishonesty a business management risk. It's on you, the owner, to control this through rigorous background checks, secure procedures, and vigilant oversight. Covering it under a standard policy could create a "moral hazard," where a business might become less careful about preventing internal theft. To close this dangerous gap, you need a separate type of coverage called a fidelity bond or an employee dishonesty policy, which can often be added as an endorsement.

How Jewelry Store Insurance Companies Calculate Your Premium

When you get a quote for Jewelers Block insurance, that final number isn't just pulled out of thin air. Instead, jewelry store insurance companies act like meticulous risk assessors, analyzing every facet of your business to land on a premium that actually reflects your unique situation. It's a detailed underwriting process, plain and simple.

Think of it like getting a home insurance quote. A house in a high-crime area with no security system is always going to cost more to insure than one in a gated community with top-of-the-line alarms. The same logic applies to your jewelry business—your operational choices and security measures directly impact the price you pay.

The global jewelry insurance market has been growing, valued at around USD 4.5 billion in 2023 and expected to hit USD 5.28 billion by 2025. This tells us one thing: more and more jewelers are getting serious about protecting their valuable assets, which makes understanding how premiums are set more crucial than ever. To dig deeper, you can discover more insights about the growing jewelry insurance market on datainsightsmarket.com.

This infographic gives a great visual breakdown of what a standard Jewelers Block policy doesn't typically cover, something every jeweler needs to be crystal clear on.

As you can see, insurers are focused on covering verifiable, event-driven losses, not issues that come from internal control problems or circumstances you can't prove.

Your Inventory Value and Composition

Let's start with the biggest piece of the puzzle: the total value of your inventory. A store carrying $5 million in diamonds and luxury watches is a fundamentally different risk than one with $500,000 in sterling silver. Insurers need a detailed, up-to-date inventory list to get a handle on their maximum potential loss.

But it’s not just about the total dollar amount. The type of inventory you carry matters, too. For instance:

- High-Value, Portable Items: A large stock of loose diamonds or high-end watches is seen as a higher risk. Why? Because they're easy for thieves to conceal and sell quickly.

- Lower-Value, Bulky Items: Larger, less valuable pieces might present a lower theft risk, and your premium can reflect that.

An accurate and detailed inventory is the bedrock of a fair quote. Without it, you can't even begin to Get a Quote for Jewelers Block.

Security Systems and Physical Protections

Your security setup is your first line of defense, and believe me, insurers notice. They absolutely reward businesses that invest heavily in it. A well-protected store is less likely to suffer a major loss, which translates directly into a lower premium.

Underwriters will look closely at:

- Safes and Vaults: They're looking for UL (Underwriters Laboratories) ratings. A high-rated TRTL-30×6 vault—which offers tool, torch, and explosives resistance—is going to earn you a much better rate than a simple residential-grade safe.

- Alarm Systems: A central station-monitored alarm is the industry standard. It should have multiple layers of protection, like motion sensors, glass-break detectors, and panic buttons.

- Surveillance Cameras: High-definition, 24/7 video surveillance with off-site backup is a powerful deterrent. It also provides priceless evidence if you ever need to make a claim.

A robust, layered security system is the most powerful tool a jeweler has to control their insurance costs. It demonstrates to underwriters that you are a proactive partner in risk management.

Business Location and Claims History

Where your store is located plays a huge role. Insurers use geographical data to assess the crime risk in your specific area. A store in a zip code with a high rate of commercial burglaries will naturally face higher premiums than one in a low-crime suburban mall.

Your business's claims history is just as important. A jeweler with a clean record over five or more years is seen as a low-risk client. On the other hand, a history of frequent claims, especially for theft, signals a higher risk. That will almost certainly lead to higher premiums or even make it tough to get coverage at all.

A specialized agency like First Class Insurance Jewelers Block Agency knows how to present these factors in the best possible light. For a detailed breakdown, you can explore our guide to jewelry store insurance cost. By understanding what jewelry store insurance companies are looking for, you can take control of your risk profile and, ultimately, your premiums.

Actionable Steps to Lower Your Insurance Costs

While Jewelers Block insurance is a non-negotiable cost of doing business, your premium isn't set in stone. The price you pay is something you can directly influence.

By taking smart, proactive steps to manage your risk, you can significantly lower your insurance costs. Leading jewelry store insurance companies actively reward jewelers who prove they're serious about loss prevention. Think of these measures less as expenses and more as investments—each one strengthens your defenses and makes you a much more attractive, lower-risk client to insurers.

Fortify Your Physical Security

Your store's physical defenses are the first thing an underwriter looks at. A strong, layered security system sends a clear message: you're a partner in managing risk. This almost always translates into lower premiums.

It all starts with your core hardware. Insurers look closely at the quality and rating of your equipment.

- Install High-Quality Safes and Vaults: Your main safe needs to be UL-rated, period. A TL-30 rated safe (tool-resistant for 30 minutes) is a solid baseline, but upgrading to a TRTL-30×6 (tool and torch resistant) vault will earn you a much better rate.

- Implement a Layered Alarm System: A basic alarm just doesn't cut it anymore. Your system needs central station monitoring and should have multiple trigger types—think motion sensors, glass-break detectors, door contacts, and panic buttons.

- Utilize HD Video Surveillance: You need high-definition cameras covering every entry point, your display cases, and the safe area. Make sure the system records 24/7 and has an off-site or cloud backup so criminals can't destroy the evidence.

A layered security approach is like having multiple lines of defense. If one layer is breached, another is ready to detect and deter the threat, minimizing the potential for a catastrophic loss and lowering your perceived risk to insurers.

Refine Your Operational Procedures

Hardware is only half the battle. Your daily routines and staff protocols are just as critical in an underwriter's evaluation. Consistent, buttoned-up procedures show a culture of security that reduces the chance of both theft and internal fraud.

Start by documenting and enforcing strict operational rules. This makes sure every team member knows their role in protecting your assets.

- Enforce Secure Opening and Closing Routines: Always have at least two employees present for opening and closing. Your checklist should include inspecting all locks, checking the premises for anything unusual before anyone enters, and confirming the alarm is set correctly when you leave.

- Maintain Strict Inventory Management: Perform regular, documented inventory counts. This isn't just about spotting discrepancies early; it shows insurers you're vigilant about preventing unexplained shortages.

- Conduct Thorough Employee Background Checks: This is a fundamental step. Before you hire anyone, run a comprehensive background check. It's one of the best ways to prevent internal theft—a risk that a standard Jewelers Block policy often won't cover.

- Manage Digital Risks: Your risk isn't just physical anymore. If you sell online, using services like Stripe's chargeback protection acts like an insurance policy for your digital sales, directly cutting down on potential losses.

By putting these steps into practice, you aren't just crossing your fingers for a lower premium—you're actively earning it. These strategies make you a far more desirable client for the best jewelry store insurance companies.

Choosing the Right Jewelry Store Insurance Company

Choosing a partner to protect your life's work is one of the biggest decisions you'll ever make. Let's be clear: not all jewelry store insurance companies are the same, and the right fit goes way beyond the price tag on the policy. When a crisis hits, your insurer is your financial first responder. You need to vet them thoroughly.

Think of it like hiring a master diamond cutter. You wouldn't hand a priceless rough stone to just anyone. You'd find a specialist with proven skills, deep expertise, and a flawless reputation. The same exact principle applies here. You need a partner who lives and breathes the unique pressures and risks of the jewelry world.

Key Criteria for Evaluating Insurers

Before you even glance at a policy document, you need to size up the company behind it. Your search should zero in on a few non-negotiable pillars of quality and reliability.

These are the core attributes that separate the adequate providers from the truly exceptional partners who will actually be there when you need them most.

- Financial Strength: Look for an A.M. Best rating of "A" (Excellent) or higher. This is basically a credit score for insurance companies, and it tells you if they have the financial muscle to pay claims, even after a catastrophic event.

- Industry Expertise: Does this company actually specialize in the jewelry industry? A generalist insurer simply won't get the nuances of inventory valuation, off-premises risks, or the specific security measures that matter. A specialist, like First Class Insurance Jewelers Block Agency, already speaks your language.

- Claims Handling Reputation: A policy is only as good as the company's track record for paying claims fairly and quickly. Dig around, ask for references, and find out what their process looks like before you ever have a loss.

Choosing an insurer is an act of trust. You are trusting them with the future of your business. That trust must be earned through a proven track record of financial stability, industry knowledge, and unwavering client advocacy.

Essential Questions to Ask Potential Insurers

Once you've shortlisted a few specialized jewelry store insurance companies, it's time to dig in. The answers to these questions will tell you everything you need to know about their real-world expertise and how they treat their clients.

- "Walk me through your process for a major theft claim." A solid partner will have a clear, structured plan to help you navigate everything from the initial report to the final settlement.

- "Can you connect me with a few other jewelers you insure?" A confident, reputable insurer will be more than happy to provide references from long-time clients in your industry.

- "How do you help your clients with risk management and loss prevention?" The best insurers are true partners. They offer practical advice on security upgrades and procedures that can prevent losses and even lower your premiums over time.

The jewelry insurance market has some major players, like Travelers and Liberty Mutual, which keeps things competitive. This has pushed the industry forward, with a surprising 64% of policies now being purchased online. You can read the full research about trends in the jewelry insurance market to see where things are headed.

Finding the right partner is the final, most important step in building a real shield around your business. When you work with a specialist who understands your world, you get more than a piece of paper—you get genuine peace of mind. The next logical step is to Get a Quote for Jewelers Block from an expert who can build the precise protection your business deserves.

Answering Your Top Jewelers Block Questions

When you start digging into Jewelers Block insurance, a few key questions always come up. It's one thing to know you need coverage; it's another to understand how it works day-to-day. Here are some quick, straightforward answers to the things jewelers ask us most.

Does My Policy Cover Mysterious Disappearance?

This is a big one. Mysterious disappearance—when a piece just vanishes with no clear sign of a break-in or theft—is a tricky area. Many standard policies will actually exclude it.

However, a true specialist in jewelry store insurance knows this is a real-world risk. They'll often offer it as an add-on, or endorsement, to your main policy. Just be prepared for it to come with its own, usually higher, deductible. It's absolutely crucial to talk this specific scenario over with your agent.

How Does Inventory Valuation Affect My Policy?

The way you value your inventory is the bedrock of your policy. You've got two main routes: "actual cash value" (what it cost you, minus depreciation) or "replacement cost" (what it would cost to get a similar new item today). Insurers will demand clean, detailed records to back up whatever value you claim.

Getting this wrong is a costly mistake. If you underinsure your stock, a major loss could leave you unable to recover. But if you over-insure, you're just throwing money away on premiums for coverage you can't even use. Keeping your inventory data accurate isn't just paperwork—it's essential for fair pricing and a painless claims process.

Ultimately, the goal is to make sure you're compensated correctly without paying for more insurance than you need.

What Happens If a Customer's Jewelry Is Stolen From My Shop?

A well-built Jewelers Block insurance policy isn't just about protecting your own stock. It must include what's known as "property of others" or "bailee" coverage. This is what kicks in if a customer's piece—whether it's in for a repair, an appraisal, or on consignment—is stolen or damaged while in your care.

This part of your policy covers the financial hit up to a set sub-limit. But honestly, its real value is in protecting your reputation. Handling a situation like that professionally and financially is how you maintain the trust you've spent years building with your clientele.

Navigating the world of jewelry store insurance requires a partner who lives and breathes this industry. First Class Insurance specializes in crafting Jewelers Block policies that provide the robust protection your business and legacy deserve. Get a Quote for Jewelers Block and secure your peace of mind today.