If you're in the jewelry business, you know your inventory isn't just stock—it's your life's work, condensed into high-value, portable assets. A standard business policy might cover your display cases and your storefront, but what about the diamonds, watches, and gemstones inside? That's where it falls dangerously short.

Jewelers Block insurance is the only real answer. It’s a specialized, all-risk policy built from the ground up to protect a jewelry business from the unique, high-stakes threats it faces every day. This isn’t just about what’s in the safe; it's about protecting your inventory wherever it goes—in transit, at a trade show, or out with a salesperson.

Understanding Jewelers Block Insurance

Think of your business as a fortress and your inventory—the diamonds, gemstones, watches, and finished pieces—as the treasure inside. A normal business insurance policy might protect the fortress walls (your building), but it does almost nothing to secure the treasure itself, especially once it leaves the premises.

This is where the game changes. A Jewelers Block policy is like a comprehensive, modern security system for that treasure. It’s designed to cover your inventory from nearly every angle, bundling multiple coverages into one seamless policy that understands the realities of the jewelry world.

It’s built on the knowledge that your most valuable assets are constantly on the move and exposed to a very specific set of risks.

Why Standard Insurance Just Doesn't Cut It

A regular Business Owners Policy, or BOP, is fine for a coffee shop or a clothing store. For a jeweler, it’s full of holes. These policies come with rigid limits and exclusions that create massive, unacceptable risks for anyone dealing in high-value gems and metals.

For starters, a typical BOP has cripplingly low limits for theft. It might be enough to cover a few stolen laptops, but it won’t even begin to cover the loss of a single high-end diamond bracelet.

Then there's the problem of location. General policies almost always restrict coverage to property inside your listed business address. The moment your inventory is in transit, at a trade show, or with a traveling salesperson, you’re often completely unprotected. They also fail to account for industry-specific risks like employee dishonesty involving high-value pieces or "mysterious disappearance"—when an item simply vanishes without any clear evidence of what happened.

To truly see the difference, it helps to compare them side-by-side. A standard BOP is designed for the average business, while Jewelers Block is tailored for the specific, high-stakes world of jewelry.

Jewelers Block vs. Standard Business Owners Policy (BOP)

| Coverage Aspect | Jewelers Block Insurance | Standard Business Owners Policy (BOP) |

|---|---|---|

| Inventory Coverage | All-risk coverage for high-value inventory like diamonds, gems, precious metals, and fine watches. | Low, capped limits on valuable items, often excluding jewelry or classifying it as "fine art" with minimal coverage. |

| Off-Premises Protection | Covers inventory anywhere: in transit, at trade shows, with sales reps, or at a customer's home. | Extremely limited or no coverage for property once it leaves the business premises. |

| Theft Protection | High limits specifically for robbery, burglary, and even mysterious disappearance. | Very low sub-limits for theft, often completely inadequate for even a small jewelry loss. |

| Employee Dishonesty | Includes coverage for theft by employees, a critical risk in the jewelry industry. | Typically excluded or requires a separate, often limited, crime policy rider. |

| Valuation Method | Agreed Value or Selling Price, ensuring you're compensated for the true market or retail value. | Actual Cash Value (ACV), which deducts for depreciation and rarely covers the full value of jewelry. |

| Specialized Risks | Covers unique perils like certified mail loss, show window damage, and damage during repair work. | Does not recognize or cover these industry-specific risks, leaving major gaps. |

As you can see, relying on a standard policy is like trying to guard a vault with a bicycle lock. It just isn't built for the job.

A Jewelers Block policy is specifically designed to close these critical gaps. It recognizes that a jeweler's assets aren't just static inventory; they are dynamic, high-value goods that demand constant, specialized protection, no matter where they are.

Ultimately, this kind of coverage is a cornerstone of effective risk security management. It’s not just about bouncing back from a loss; it's the financial backstop that gives you the confidence to operate in such a high-stakes industry. That’s why working with a specialist like First Class Insurance Jewelers Block Agency is so crucial—we live and breathe the specific risks you face every day.

You can Get a Quote for Jewelers Block to see exactly how this essential coverage can be shaped to protect your business.

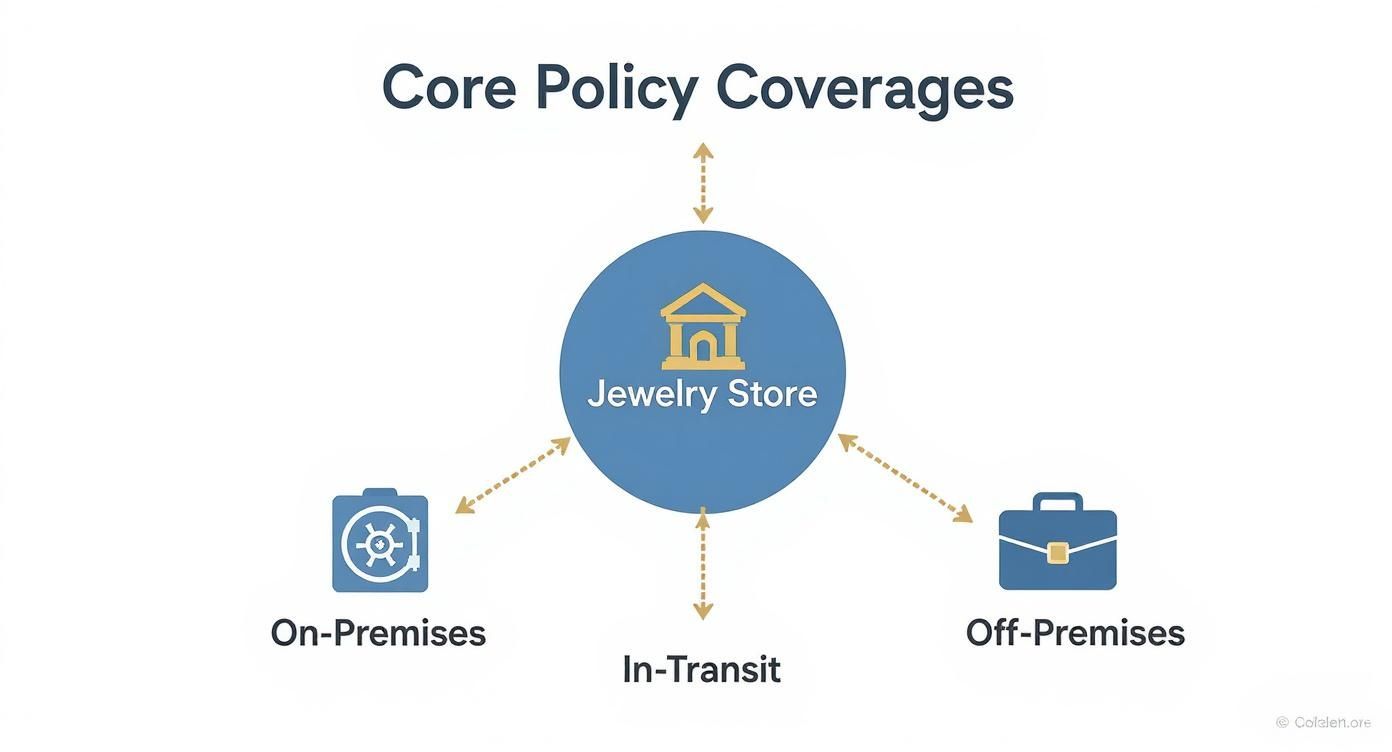

Understanding Your Core Policy Coverages

Think of a Jewelers Block policy less like a single shield and more like a custom-fitted suit of armor. It’s built with interlocking pieces, each one designed to guard against a specific threat your business faces every single day. This isn't about abstract terms; it's about real, tangible security for your inventory, whether it's sitting in the vault, traveling across the country, or sparkling under the lights at a trade show.

Let's break down these core protections piece by piece, using scenarios every jeweler knows all too well.

On-Premises Protection For Your Storefront

Your store is your fortress, but even the most secure locations have weak points. On-premises coverage is the absolute foundation of your policy, protecting the inventory and other precious property sitting inside your physical shop. It goes way beyond what a standard business policy would ever dream of covering.

Picture a classic smash-and-grab. A thief shatters your display case after hours and snags a tray of diamond rings. This is exactly what on-premises coverage is for—it’s designed to respond immediately and cover the cost of that stolen merchandise.

But it’s not just for the dramatic stuff. What if a pipe bursts and floods your showroom, ruining delicate settings and customer repairs? On-premises coverage is your backstop for losses from fire, water damage, and other physical disasters that can devastate your stock.

Key Takeaway: This coverage protects the full value of your stock, raw materials, and even customers' pieces left in your care while they're on your property. It's your first and most vital line of defense.

In-Transit Coverage For Goods On The Move

Jewelry is rarely meant to stay in one place. It moves constantly—between suppliers, appraisers, setters, and of course, your customers. Jewelers Block insurance is built for this reality, offering strong in-transit coverage that protects your assets the second they leave your four walls.

Imagine you're sending a parcel of loose stones to a buyer using an approved armored courier. You've done everything right, but the shipment simply vanishes. It’s declared lost.

Without this specialized coverage, a loss like that could be a financial knockout punch. In-transit protection steps in to cover these exact situations, making sure you’re compensated for the full value of goods lost while being shipped by couriers, USPS Registered Mail, or even when carried by you or your sales team. It's what lets you keep your business moving without the constant fear of a shipment disappearing.

Off-Premises Security For Shows and Sales

So much of this business happens outside the store. Whether you're at a huge trade show in Vegas, a private viewing in a client's home, or a local trunk show, your inventory is at its most vulnerable. Off-premises coverage extends your policy's protective bubble to these high-risk, high-reward environments.

Here's a scenario that gives jewelers nightmares: you’re at a busy trade show, deep in conversation with a promising buyer. In that split second of distraction, a professional thief swaps a genuine diamond necklace with a worthless replica.

This kind of sophisticated, sleight-of-hand theft is a massive risk at shows. Off-premises coverage is built to protect you from theft, loss, or damage when your inventory is away from your main location. It gives you the freedom to showcase your best pieces with confidence, knowing your financial backbone is secure. For a deeper look at what’s included, you can learn more about what Jewelers Block insurance covers in our detailed guide.

Protection Against Internal Threats

Not every threat comes from outside your walls. It's a tough pill to swallow, but employee dishonesty is a serious risk in any business handling high-value, portable assets. This coverage, either included or added as a critical endorsement, shields your business from theft committed by your own team.

Think about an employee with access to the safe who starts pocketing small items over several months, carefully fudging the inventory records to cover their tracks. By the time you notice, the loss could be enormous—we’ve seen documented cases climb past $100,000.

This coverage is designed to reimburse you for those kinds of losses, giving you a crucial safety net against a devastating betrayal of trust. It’s an uncomfortable topic to discuss, but it's a non-negotiable protection for your business.

How Policy Limits and Valuations Really Work

It’s one thing to know what your Jewelers Block insurance covers, but understanding the financial side—how you actually get paid after a loss—is just as critical. The payout you receive hinges entirely on your policy limits and the method used to value your inventory.

Getting these details right can mean the difference between a manageable hiccup and a business-ending catastrophe.

Think of your policy limits as the ultimate financial backstop your insurer provides. These numbers aren't pulled out of thin air; they are specific caps on how much your policy will pay for a single event and over the entire year. Let’s break down the two main limits you need to know.

- Per-Occurrence Limit: This is the absolute maximum your policy will pay out for any single incident. If a thief makes off with $750,000 in merchandise, but your per-occurrence limit is set at $500,000, the insurance payment stops there. You’re left on the hook for the remaining $250,000.

- Aggregate Limit: This is the total ceiling for all claims filed within your policy period, which is typically one year. Even if you have several smaller claims that are each under your per-occurrence limit, the total payout for the year can’t go past this aggregate number.

These limits create the financial framework for your coverage. The infographic below shows how the core protections—on-premises, in-transit, and off-site—all operate within this structure.

As you can see, every stage of your operation is protected, but always subject to the limits and valuation methods spelled out in your policy.

Choosing The Right Valuation Method

Beyond limits, the valuation method is arguably the most important piece of the puzzle. It determines how the insurance company calculates the worth of a lost or damaged item. Pick the wrong one, and you could get a check that doesn't even come close to covering your true loss, especially for custom or one-of-a-kind pieces.

This is where practices like pre-authentication for reducing claims costs are becoming so important, as they help lock in clear values before a loss ever happens.

There are three common ways to value property, but for a jeweler, only one really makes sense.

- Actual Cash Value (ACV): This is the most basic method, and it's a huge gamble for any jeweler. ACV pays you the replacement cost minus depreciation. Since jewelry trends evolve and certain cuts or styles can be perceived as "dated," an ACV calculation could seriously undervalue a beautiful vintage piece.

- Replacement Cost: This is a much better option. It covers the cost to replace the stolen item with a new, similar one, without any deduction for depreciation. The problem? For custom work or truly unique gemstones, a "similar" replacement might not exist, failing to capture the item's real market value.

The Gold Standard: Agreed Value

For anyone in the jewelry business, Agreed Value is the only way to go. With this method, you and your insurer agree on the value of your inventory—either item-by-item or as a whole collection—before the policy even starts. If a covered loss occurs, the insurer pays that exact, pre-determined amount. No arguments, no last-minute appraisals.

Why Agreed Value Is Non-Negotiable

Agreed Value simply erases the doubt and negotiation that can happen during a claim. It ensures your high-margin, custom, and one-of-a-kind pieces are valued for what they're truly worth in the market, not just for the sum of their parts.

For a business built on unique artistry and value, this isn't a luxury; it's essential.

When you Get a Quote for Jewelers Block, insisting on an Agreed Value clause is one of the most important moves you can make. At First Class Insurance Jewelers Block Agency, we make this a priority, building policies that reflect the true, tangible value of our clients' life's work.

Getting Familiar With Policy Exclusions and Conditions

While a Jewelers Block insurance policy is incredibly comprehensive, it’s not a magic wand. No policy covers absolutely everything, and understanding what isn't covered is just as critical as knowing what is.

Think of these exclusions not as hidden traps, but as clear boundaries. They’re there for a reason—often to prevent fraud or discourage risky behavior. Getting to know them helps you tighten up your own security and avoids the heartbreak of a denied claim right when you need the help most.

Why Some Losses Aren't Covered

Insurers write policies to cover clear, definable events—a smash-and-grab, a fire, a shipping mishap. They draw the line at situations that are ambiguous, preventable through basic care, or smell of potential fraud.

Here are a few classic exclusions you'll run into:

- Unattended Vehicle Losses: This is a big one. A salesperson leaves a case of Rolexes in the car while grabbing a quick coffee, and the car gets stolen. That loss is almost certainly not covered. To an insurer, leaving high-value inventory in an unattended vehicle is an open invitation for theft.

- Voluntary Parting: This happens when you’re tricked into willingly giving an item away. A scammer pays with a bad check that looks real, or a con artist spins a convincing tale and walks out with a diamond bracelet. Because you handed it over, it falls outside the typical definition of theft.

- Mysterious Disappearance: This is probably the most common point of confusion. It’s when inventory is simply gone during a stock count. There’s no sign of a break-in, no security footage of a theft—the item just vanished.

From an insurer's perspective, a mysterious disappearance points to a weakness in inventory management, not a specific, insurable event. Without proof of what happened, they can't verify the loss.

This is where airtight inventory controls become your best friend. A modern system using RFID tags or even diligent daily spot checks can help you pinpoint when an item went missing, which can be the key to turning an unprovable "mysterious disappearance" into a documented, coverable theft.

The "Must-Do" Rules: Policy Warranties

Beyond exclusions, your Jewelers Block policy will have warranties. These aren't suggestions; they are hard-and-fast promises you make to your insurer about the security measures you will always have in place.

Breaking a warranty can be a deal-breaker, potentially voiding your coverage for a claim that would have otherwise been paid. You have to hold up your end of the bargain. While your policy can offer incredible protection, like worldwide coverage or extended limits, it's all built on a foundation of trust that you're following these rules. For a deeper dive, you can explore more about how these specialized policies are structured at RPSins.com.

Common warranties include things like:

- Safe and Vault Requirements: Your policy will spell out exactly what kind of safe (e.g., a TL-30 rated vault) must be used to store high-value inventory when you're closed.

- Alarm System Functionality: You promise that your alarm system will always be on, professionally monitored, and kept in good working order.

- Out-of-Safe Limits: You agree that the total value of inventory left out of the safe overnight will never go above a specific dollar amount.

The consequences for not following these are severe. If you have a burglary but forgot to arm the alarm that night, the insurer can legally deny the entire claim. You breached a warranty. This is exactly why working with an expert at First Class Insurance Jewelers Block Agency is so important—we make sure you understand every single condition before you sign, so your protection is always rock-solid.

How Insurers Calculate Your Premiums

Ever peeked behind the curtain to see how an insurer lands on your specific premium for Jewelers Block insurance? It’s far from a one-size-fits-all number. Think of underwriters as risk detectives. They meticulously investigate every angle of your operation to build a premium that mirrors your unique risk profile.

Knowing what they look for is a game-changer. It puts you in the driver's seat, showing you exactly where strategic business decisions can directly lower your insurance costs.

Your Inventory Profile

No surprise here: the single biggest factor driving your premium is your inventory. But it's not just about the total dollar value. Underwriters dig much deeper, analyzing the type of merchandise you keep on hand, because some items are just plain riskier than others.

A wholesaler dealing in loose, high-value diamonds is a completely different animal than a retailer specializing in sterling silver. Why? Loose stones are tiny, incredibly valuable, and much easier for a thief to pocket and sell off. That makes them a higher-risk category.

Key Takeaway: Your premium is directly tied to both the total value and the makeup of your inventory. A higher concentration of easy-to-grab items like loose gems and luxury watches will almost always mean higher rates.

Physical and Procedural Security

Next, the underwriter sizes up your fortress. Just how secure is your physical location? This is one of the most critical parts of their evaluation, and it’s an area where your investments can pay off in a big way.

They’ll want to know everything about your security setup:

- Safes and Vaults: The rating on your safe speaks volumes. A TL-30 or TRTL-30×6 vault screams "serious about security" and earns you a lot more trust (and better rates) than a basic safe. Upgrading your vault is often one of the quickest ways to see a drop in your premium.

- Alarm Systems: A professionally installed and monitored alarm is a must. Underwriters look for systems with redundant communication (like a cellular backup) and sensors on every possible point of entry.

- Surveillance: High-definition cameras, both inside and out, aren't just for show. They act as a powerful deterrent and give you critical evidence if something does happen.

- Access Controls: Simple things, like how you manage keys and codes or your protocols for opening and closing, all paint a picture of your risk level.

Investing in top-tier security isn't just about stopping thieves—it's about demonstrating to your insurer that you're a low-risk partner. That proof translates directly into savings.

Operational Risks and Business Location

How you do business and where you do it also play a huge role in shaping your premium. If your business is constantly on the road for trade shows or has a team of traveling salespeople, your off-premises risk is significantly higher than a single-location retailer. Underwriters have to account for that increased potential for loss while your inventory is in transit or at a show.

Your shop’s physical address matters, too. A store in a high-crime neighborhood will naturally face higher premiums than one in a quiet suburban spot. Insurers use massive amounts of data to assess the crime rates and specific risk factors tied to your zip code.

Finally, your claims history is your report card. A business with a history of frequent losses—even small ones—looks like a higher risk and will probably pay more than a business with a clean slate. This makes solid loss prevention not just a good practice, but a core part of your long-term financial strategy.

The cost for Jewelers Block Insurance can vary quite a bit, but typically falls between 0.5% and 3% of your total insured value each year. For example, a retailer with $500,000 in inventory might see premiums anywhere from $2,500 to $15,000 annually, with the final number depending on their security, location, and loss history.

To get a much clearer picture of what your specific costs might look like, take a look at our guide on how much Jewelers Block insurance costs. At First Class Insurance, we can help you make sense of all these factors and get a quote that truly reflects your commitment to security.

Securing Your Tailored Jewelers Block Policy

Okay, you've learned the ins and outs of Jewelers Block insurance. Now comes the most important part: moving from theory to action and getting a policy that actually protects your life's work. This isn't just about filling out an application; it's about forging a partnership with an expert who genuinely gets the unique pressures of the jewelry world.

This is where a specialist truly makes all the difference. A general insurance agent might mean well, but they often see your business through the same lens as a restaurant or a retail shop. They simply don't have the deep-seated knowledge to spot the subtle—but critical—risks that define the jewelry trade. That lack of expertise can leave you with dangerous gaps in your coverage or, just as bad, a bloated policy full of expensive add-ons you'll never use.

The Value of a Specialist Agency

Partnering with a dedicated agency like First Class Insurance Jewelers Block Agency is a completely different ballgame. We live and breathe the challenges you face every single day, whether it's securing a million-dollar inventory at a trade show or managing the risk of employee access to high-value pieces. We don't just sell insurance; we help you construct a financial shield that's custom-fit to your operation.

Here’s how we do it:

- A Deep-Dive Risk Assessment: We move past the surface-level questions to truly understand your security protocols, what your inventory looks like, and how your business actually runs.

- Custom Policy Design: We'll help you dial in the right limits, add the necessary endorsements, and choose the valuation methods that make sense, ensuring you're never left underinsured when it matters most.

- No-Nonsense Quote Explanations: We walk you through every line item. You'll know exactly what's covered, what isn't, and why, so there are no surprises down the road.

This meticulous approach means your policy is a perfect fit. It gives you robust protection without making you pay for coverage you just don't need.

Working with an expert means you gain an advocate who understands the nuances of jewelry risk. This partnership ensures that when a loss occurs, your policy is built to respond exactly as you expect it to.

Your Next Steps to Full Protection

You’ve poured years of passion, sweat, and capital into building your business. The final, crucial step is to protect that investment with coverage designed by people who know your world inside and out. Don't leave your future to chance with a generic, one-size-fits-all policy.

If you're still weighing your options, our guide on if you need a Jewelers Block policy can offer some more clarity.

Ready to take control of your business’s security? The process is straightforward. Get a Quote for Jewelers Block from First Class Insurance today and let our specialists build the customized protection your jewelry business deserves.

Frequently Asked Questions

When you're dealing with something as specialized as Jewelers Block insurance, questions are bound to pop up. We get it. Here are some of the most common ones we hear from jewelers just like you, with straight-to-the-point answers.

Is Jewelers Block Insurance Required By Law?

No, you won't get a fine for not having it—it’s not a legal mandate like workers' comp. But let's be realistic: given the staggering value of jewelry inventory, running your business without it is like leaving the vault door wide open. It’s a financial gamble very few can afford.

Plus, many landlords and banks won't even work with you unless you have a policy in place. They often require it as a non-negotiable term for a lease or a business loan.

Does This Policy Cover Customer Property?

Absolutely. In fact, this is one of the most critical parts of a solid policy. It protects the watches, rings, and other pieces your customers leave with you for repair, appraisal, or consignment.

This isn't just about covering a loss; it's about protecting your reputation. Having this coverage in place shows your clients you're a true professional who takes responsibility for their cherished items.

Think of it this way: a good policy doesn't just protect your inventory. It also covers "property of others in your care, custody, or control," which is the industry's way of saying, "We've got your customers' valuables covered, too."

Can I Get Coverage For Just One Event?

You can, but it’s rarely the best move. While some carriers offer temporary coverage for a single trade show or exhibit, it’s a bit like putting a band-aid on a problem that needs a full suit of armor.

A comprehensive annual Jewelers Block policy is designed to protect you 24/7, whether your inventory is in the safe, on display, or heading to a show. Trying to patch together event-specific policies often creates dangerous coverage gaps and can end up costing you more in the long run.

What Should I Do If I Need To File A Claim?

Experiencing a loss is stressful, but knowing what to do next can make all the difference. The first few moments are crucial.

Here’s your immediate action plan:

- Safety First: Before you do anything else, make sure you and your team are safe.

- Call the Police: If there's been a crime, like a robbery or break-in, report it immediately. Get a copy of the police report—you'll need it.

- Document Everything: Pull out your phone. Take pictures and videos of any damage. Start making a detailed list of every single item that's missing or damaged.

- Notify Your Agent: Call us at First Class Insurance Jewelers Block Agency right away. The sooner you let us know, the faster we can start the claims process and guide you through every step.

Your business is a unique blend of artistry, trust, and incredibly valuable assets. Protecting it isn't just another expense; it's one of the most important investments you'll make. Here at First Class Insurance, our specialists live and breathe this industry. We're ready to build a policy that fits your business like a custom-made setting.

Ready to secure your legacy? Get a Quote for Jewelers Block and let's build the right protection together.